Record CfD Subsidies in 2024

A record £2.4bn in CfD subsidies paid in 2024

Introduction

Hot on the heels of the record payments made under the Feed-in-Tariff scheme in the year to end March 2024, the data is now available for subsidies paid under the Contract for Difference Scheme (CfDs) in calendar year 2024. The data comes from the Low Carbon Contract Company (LCCC). The data is subject to minor revision and the data snapshot for this piece was taken on 14th January 2025.

A record £2.4bn was paid out in subsidies across a range of technologies, but the largest recipient was offshore wind. There are some other interesting facts buried in the data that we can now explore.

How Do CfDs Work?

I am often asked how CfDs work, so it is worth giving a brief explanation before diving into the detail of the data. I have pulled Figure 1 below from the Renewable Exchange to illustrate how they work.

The black line shows the market price (or reference price) of electricity on any given day. The red line is the CfD strike price and reflects how much the generator will get paid for its electricity, regardless of the market value. Note that in reality, as we shall see below, the average strike price for active offshore wind CfDs is over £150/MWh.

When the black line is below the red line, the generator receives the market price for the electricity generated plus a CfD top-up (subsidy) for the difference. On the rare occasions when the market price is above the strike price, the generator pays back money to the LCCC as illustrated by the blue line, so its net revenue is equal to the strike price.

Full Year Subsidies

Figure 2 shows the full year subsidies since the scheme began in late 2016, broken down by technology type.

")

As well as 2024 being a record year overall, offshore wind received more subsidy than in any other year with £1.9bn paid out. Biomass conversion, a euphemism for burning trees, received £309m and biomass with combined heat and power (CHP) received a further £90m. Onshore wind received £73m and the two solar farms with active CfDs received just over £1m.

Incidentally, in December 2024, £260.3m was paid out in subsidies, the second highest month on record, with April 2024 being the highest at £269.8m.

Supporters of renewables often point out that when the market price of electricity is above the CfD strike price, then generators pay money back. This is true, but that was only significant in 2022 when a net £346m was repaid and compares to the net cost of the scheme of £9.6bn since inception.

Top-20 Subsidy Days

From the data, it is also possible to work out the Top-20 subsidy days since the scheme began. These are listed in Figure 3 below.

The top thirteen CfD subsidy days all occurred in 2024, and a total of 16 days from the same year all appear in the Top-20. The day with the highest subsidy payments was 22 December 2024, with over £20m paid out in a single day. Offshore wind was the main recipient of this Government mandated largesse on that day, getting over £18.3m and biomass receiving over £1m.

The record subsidy days in December last year came despite elevated gas prices pushing up the reference price. The annual indexation of CfD strike prices with inflation means that as each year progresses, we are likely to see many more record subsidy days, especially if gas-prices fall back to more normal levels.

Top CfD Subsidy Recipients

We can also see the top recipients of the subsidy largesse. The all-time Top-10 list is shown in Figure 4a below with the Top-10 for 2024 shown in Figure 4b.

Six of the all-time Top-10 recipients are offshore wind farms. Walney has received the most at £1.76bn, with Hornsea Project 1 coming in second at £1.67bn. In third place is Drax that has been paid £1.6bn in subsidy for burning trees. Note Drax also has another plant that is funded by Renewables Obligation Certificates, so this is only part of the story. The other offshore wind farms in the Top-10 are Dudgeon, Beatrice, Burbo Bank and East Anglia One. Lynemouth and Teesside Biomass plants also make the Top-10 along with the Dorenell onshore windfarm.

The 2024 Top-10 is dominated by offshore windfarms, with Drax coming in at number six with Lynemouth biomass plant in ninth place with Teesside Biomass and CHP plant in tenth place.

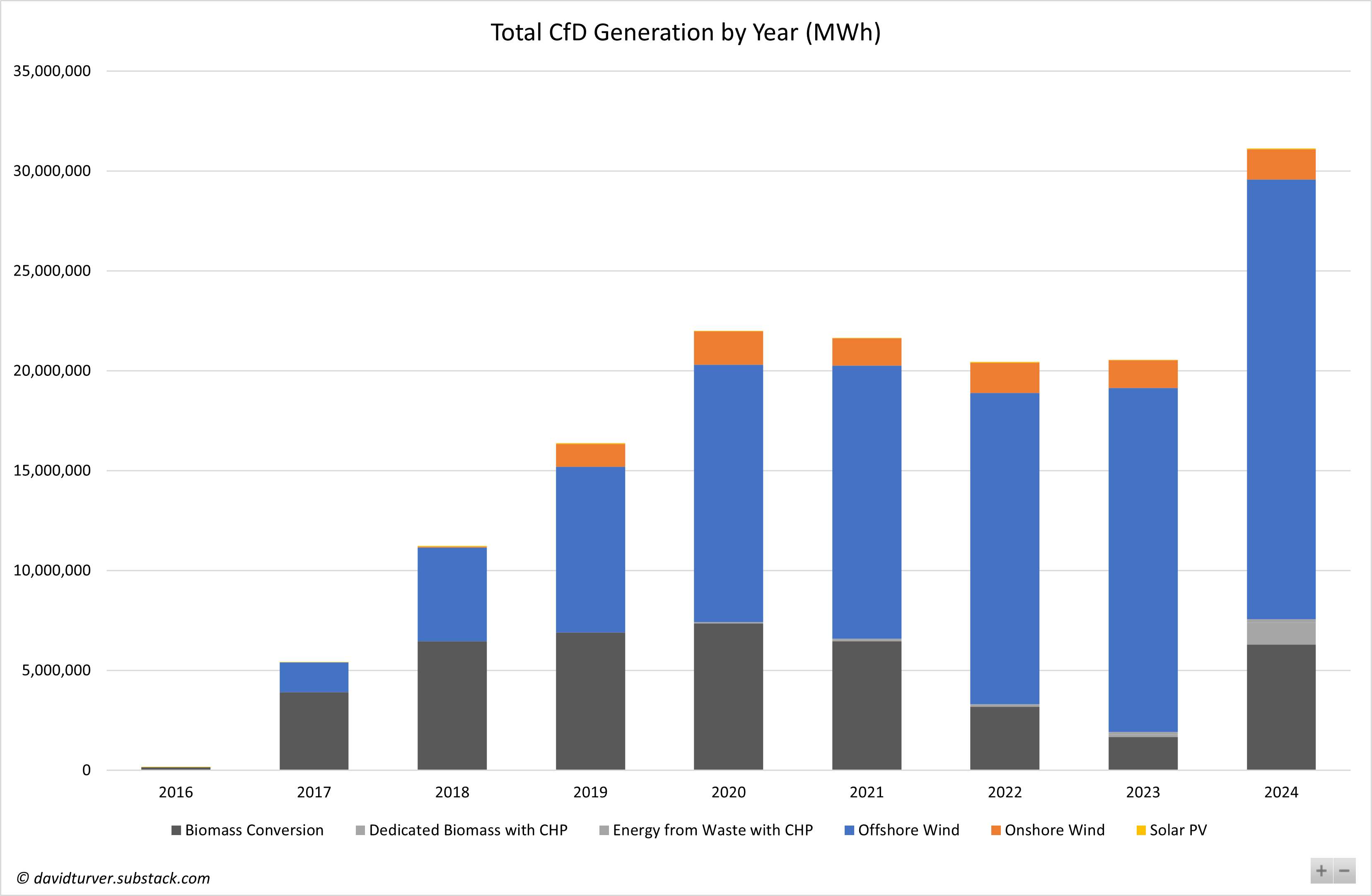

CfD Electricity Generation

We can now work to explain why the subsidy payments have been rising. To begin with, we can look at total generation as shown in Figure 5.

Generation is also hit an all-time high in 2024, with a substantial increase to offshore wind generation to another annual high due to the activation of the CfDs for Hornsea Project 2 and Moray East in March last year. Biomass and Biomass with CHP also saw considerable increase in output. There are only two active CfDs for solar power and their output is virtually undetectable.

CfD Strike Prices

As can be seen in Figure 6, in general strike prices rise over time as they get indexed up with inflation in April each year.

The strike price for Biomass has gone up each year since 2017 rising from £107/MWh to over £139/MWh last year. A similar picture emerges for onshore wind and solar. The exception is offshore wind where prices fluctuated in the £160-165/MWh range from 2017 to 2022. Then there was a big jump in 2023 to £171/MWh before falling back to £154/MWh in 2024. The drop in 2024 can be explained by Hornsea Project 2 and Moray East activating their CfDs in March 2024. The strike price for these two projects is much lower than the other projects at £78/MWh, so they brought down the average even though the strike price of the other projects indexed upwards.

CfD Reference Prices

The weighted average reference price for the year (equivalent to the black line in Figure 1) has fluctuated a lot since 2017 as shown in Figure 7.

")

The charts for offshore wind, onshore and solar are all very close, so for clarity this chart shows just the intermittent reference price for offshore wind. The various flavours of biomass use a different reference price called the Baseload Market Reference Price (BMRP) and we shall deal with separately. Average offshore wind reference prices were in the range £41-57/MWh from 2017 to 2019. Prices plummeted in 2020 as gas prices and demand fell due to Covid. Prices rose in 2021 to an average of £115/MWh mainly due to the energy crisis that began in the second half of that year. Prices rose again in 2022 to £177/MWh as the energy crisis continued with Russia’s invasion of Ukraine before falling back somewhat to £89/MWh in 2023. Prices have fallen further in 2024 to £67/MWh even though prices have been somewhat elevated in the latter part of the year.

CfD Subsidies Per MWh

The difference between the strike price and the reference price allows us to calculate the subsidies received per MWh of generation as shown in in Figure 8.

")

In 2022, all technologies paid back into the system on average, with negative subsidies per MWh generated. However, in 2023 and 2024 subsides rose back into positive territory for all three intermittent technologies.

We can see the share of market revenue and subsidy revenue for each technology in 2024 set out in Figure 9.

")

Offshore wind received subsides of £86/MWh, which is more than the intermittent reference price of £67/MWh, meaning that on average CfD funded offshore wind farms got more of their revenue from subsidies (56%) than they got from selling their power on the market. Onshore wind received £48/MWh (43%) and solar got £45/MWh (41%) of their revenue from subsides.

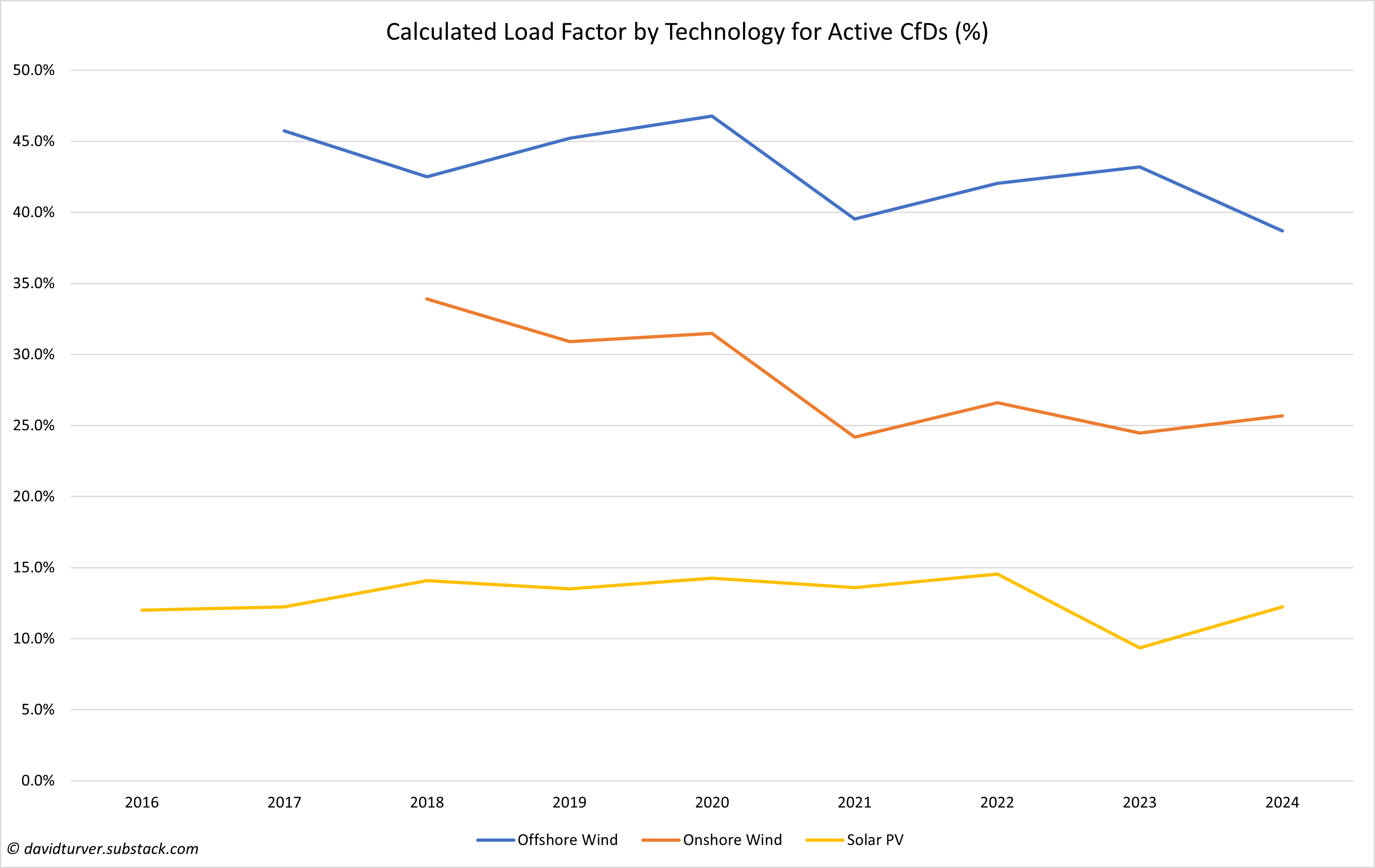

Load Factors

We can also calculate the average load factor for the main intermittent technologies funded by Contracts for Difference as shown in Figure 10.

We can see a general downtrend in the amount of electricity generated compared to nameplate capacity for all three technologies. However, offshore wind achieved a load factor of just 38.7%, the lowest on record, despite new wind farms coming online. However, the average is skewed somewhat by Moray East that had a load factor of just 21%, probably reflecting a high level of curtailment during the year. Curtailment happens when wind is producing more power than there is demand or the grid can handle, so windfarms are asked to switch off. Although Beatrice and Triton Knoll showed a big increase in load factor in 2024 compared to 2023, East Anglia 1 and Hornsea Project One both saw significant reductions.

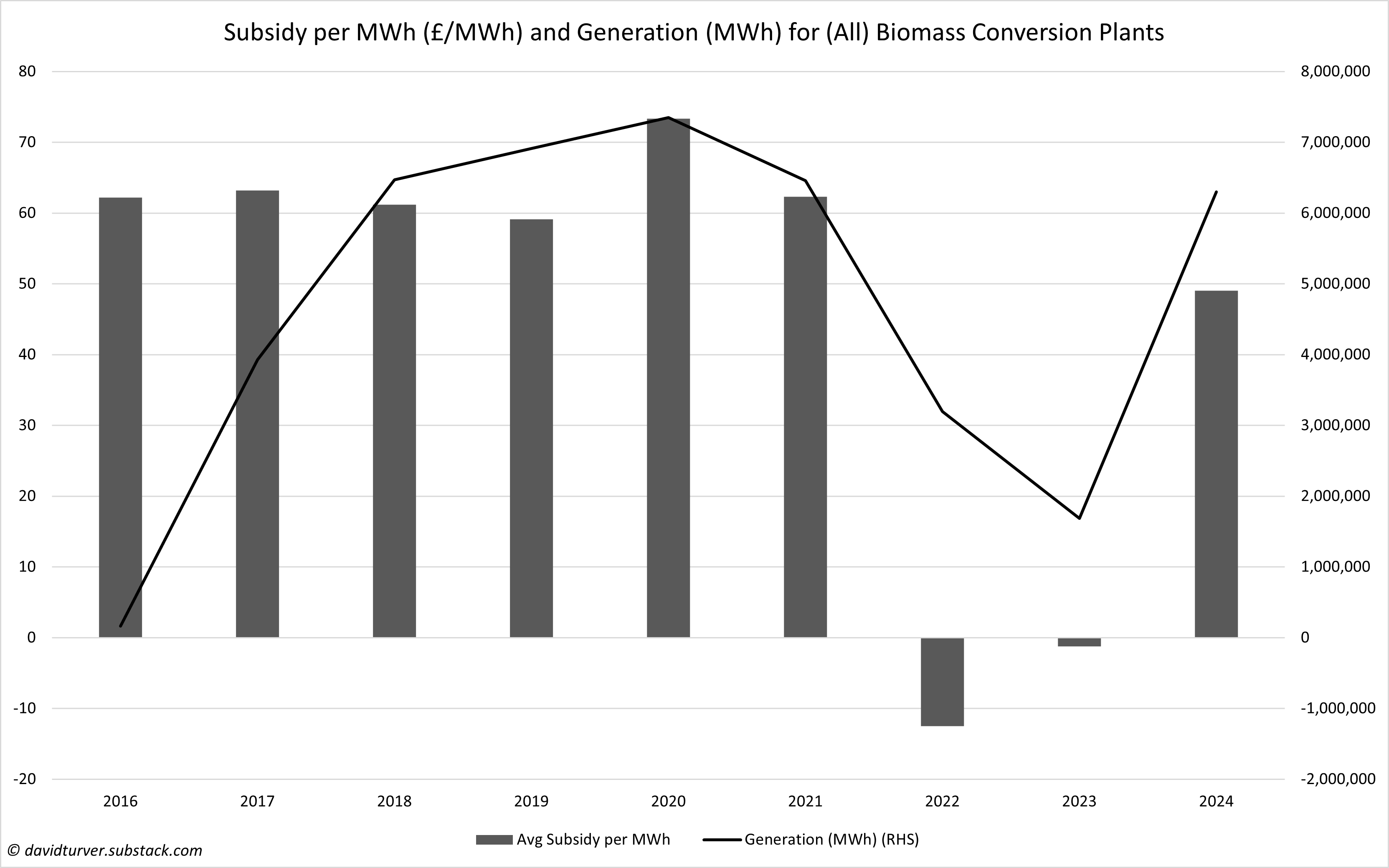

CfD Subsidies for Biomass Plants

Moving back to biomass plants, we can see how much subsidy they received per MWh of generation and the relationship between subsidies and generation in Figure 11.

Conclusions

What conclusions can we draw from all this data? It is virtually certain that the overall subsidy payments will continue to rise in the coming years because more offshore wind farms are coming on stream that will push up the level of generation.

It is more difficult to predict strike prices. However, we know that new developments coming online such as Neart na Gaoithe (NNG) where the strike price is currently £158/MWh, coupled with a new round of indexation coming in April will have the effect of pushing up the average strike price. However, other projects with lower strike prices such as Dogger Bank and Sofia may come online and activate their CfDs too which would push strike prices in the opposite direction.

Reference prices are even harder to predict because we do not know future gas-prices which are the main driver of reference prices. Higher gas prices would tend to reduce subsidies because the reference price goes up. Gas prices are currently elevated, so provided global tensions do not escalate, we might expect gas-prices to fall and therefore reference prices would fall too and subsides would rise. Moreover, putting more offshore wind on the grid tends to reduce reference prices when it is most windy. Lower reference prices would tend to increase subsidies per MWh at the time when there is most generation.

It is sad to conclude that we are in for higher bills as the bill for Contracts for Difference continues to escalate.

This Substack now has well over 3,300 subscribers. This growing interest has led to me being invited to give a talk to Sacred Cows on 28th January in London entitled “Net Zero: Why the cure is worse than the climate change disease”. More details and tickets can be found here, do come along if you can make it

If you enjoyed this article, please share it with your family, friends and colleagues and sign up to receive more content.

Not to mention the ecological devastation caused by offshore wind in particular.

Thank you David for another data-driven analysis, which deserves several readings. It has provoked some questions and observations. Can a modern energy system be built without subsidies? In particular, nuclear power, of which I am convinced on account of energy density, small land footprint, reliability and safety. Subsidies, which transfer resources (currency) from the general population to particular interests, are evil, but may be a necessary evil in order to get some things done, where there is a payoff to society, such as keeping the lights on. The UK is in the process of building the most expensive nuclear plant in the world at Hinckley Point C due to our insistence on regulating the best and safest plant ever*. Yet the guaranteed electricity price, while (too) high, is below strike prices for offshore wind. It is as though I am being commanded to pay a premium for a car that won't run in dull, windless conditions. I wouldn't volunteer a visit to that showroom.

Of course, usual reminder: on top of subsidies, we have additional costs of often inefficient backup generation and build out of grid infrastructure.

As per the old Irish navigational advice: "Well I wouldn't start from here".

* China and South Korea have shown that cost and time over-runs on nuclear plant are not a law of physics.