Alas, Poor ORIT

Despite harvesting massive subsidies, aggressive accounting policies may contribute to the downfall of the Octopus Renewables Infrastructure Trust.

Introduction

While researching earlier articles on the offshore wind decommissioning timebomb, and the recent spate of wind operator’s profit warnings I had occasion to dig into the accounts of some of the funds offering exposure to renewable energy to retail investors. There were some interesting findings from that research, so this is the first of two articles in a mini-series looking at at Octopus Renewables Infrastructure Trust (ORIT) and Greencoat UK Wind (UKW) whose share prices have been falling recently. Let’s dig in.

Share Price Performance

As we can see from Figure A, the share price has been in a long down trend since peaking in August 2022.

The share price has fallen despite paying £33.5m in dividends in 2024 and buying back £6.8m of its own shares. Share buybacks have been continuing in 2025 too.

According to their latest accounts, ORIT’s investment objective is to provide investors with an attractive and sustainable level of income returns with an element of capital growth. Dividends have risen from 3.18p/share in 2020 to 6.02p/share in 2024. But as we can see, capital growth has been lacking because the Net Asset Value (NAV) has been falling, but not as quickly as the share price.

The dividends are paid because the renewable assets that ORIT invests in harvest subsidies. At the end of 2024, ORIT had stakes in 41 different assets across five separate technologies including solar, batteries, hydrogen, onshore and offshore wind. The company’s portfolio is diversified geographically as well as across technologies.

Subsidy Harvesting

ORIT has a stake in the Lincs windfarm that has received Renewables Obligation Certificates (ROCs) worth a total of over £550m up to the end of 2024. ORIT only has a 15.5% stake in Lincs, so it will have received only a portion of the subsidies. ORIT also owns nine solar farms, of which eight are subsidised under the ROC scheme and have earned certificates worth ~£59m so far.

ORIT also owns the Cumberhead and Crossdykes onshore windfarms, which operate without direct subsidy. However, they are eligible for constraint payments. In other words, they get paid to turn off the turbines when there is more wind power than the grid can handle, or when supply exceeds demand. According to data from the Renewable Energy Foundation, these windfarms have received £7.9m in payments for what the Chief Executive of Octopus Group terms “wasted wind”. It does seem rather odd that Greg Jackson should be complaining about wasted wind when one of the Octopus investment companies is benefitting from the phenomenon.

ORIT Risks

Despite the seemingly strong and stable revenue arising from harvesting subsidies and collecting curtailment payments, there are several risks to the ORIT business model:

Diminishing assets

Rising discount rates

Falling generation

Optimistic asset life

Power price risk

Decommissioning liabilities

Debt

Diminishing Assets

First, the gross value of the assets ORIT holds fell by £6.4m to £699.6m in 2024, however net assets fell by nearly £29m to £570m primarily because of an increase in debt of more than £21m to £151m. A declining asset base is not conducive increasing dividends or capital growth.

Rising Discount Rates

In common with other funds invested in renewables, ORIT’s assets are classed as Level 3. This means that asset values are calculated by management in the absence of observable market price data. They do not disclose the full methodology, but in effect, they calculate present value of the expected cashflows from the assets over the remainder of their lives. This figure is highly sensitive to several variables such as the discount rate, inflation, electricity generation, asset life and power price.

The discount rate is linked to long-term interest rates which have been rising recently. They disclose that a 0.5% increase in the discount rate would decrease the portfolio value by 5.3%. However, any decrease in valuation caused by an increasing discount rate might be offset by rising inflation which has also been edging up. They say that an increase in inflation of 0.5% would increase portfolio values by 3.9%.

Falling Generation

Of course the volume of electricity generated impacts the asset value. They disclose that a reduction from the P50 level to the P90 level (90% probability of being exceeded) would cause a 16.1% decrease in portfolio value. In 2024, they note the Lincs windfarm in which ORIT holds at 15.5% stake suffered from breakdowns and a decline in output of 4% compared to budget.

It is interesting is that RWE, Orsted, TRIG and Greencoat UK Wind have all issued profit warnings this year because of lower than expected wind generation. Six of ORIT’s top-10 investments are in wind projects in the UK, Finland, France and Germany so it is likely that ORIT’s wind assets have also suffered reduced generation. This is not yet evidence of a trend, but short term the asset value will likely have to be reduced.

Optimistic Asset Lives

The future revenue from generation is impacted by the assumed asset life. ORIT sets asset lives on an asset-by-asset basis, but there are grounds to believe their estimates are wildly optimistic. ORIT owns 15.5% of Lincs offshore wind farm through its indirect holding in UK Green Investment Lyle Limited. ORIT’s 2024 accounts (p37) show that Lincs began operation in 2013 with a remaining asset life of 24 years, making the total asset life expectancy of 35 years. Yet, the accounts for the actual wind farm and Green Investment Lyle show an asset life of just 20 years. The ROC subsidies will run out in 2033, meaning ORIT expect it to operate for 15 years without subsidy.

These extra years of expected life enable ORIT to inflate the asset value. If we look in detail at the 2023 accounts of the wind farm we can see that revenue less EBITDA, a measure of the cash cost of operation, has risen from ~£42/MWh in 2014 to about £67/MWh in 2023. As the wind farm ages we can expect generation to decline and fixed costs to rise, so cash costs per MWh are likely to continue to rise. If they exceed the market value of the electricity generated Lincs offshore wind farm would not be economic once the subsidies run out in 2033. Their assumption of an extra 15 years of life after subsidies end looks to be shaky to say the least, especially when considering the breakdowns in 2024.

Power Price Risk

ORIT identifies changes in power prices as a risk to the portfolio valuation, noting that a movement of +/-10% in power prices will impact the NAV by +/-8.4%. Their expected realised prices are shown in Figure B below.

")

They calculate their expected realised price as a discount to expected wholesale baseload prices for each country they operate. The magenta line shows the expected raw power price and the blue line shows the total remuneration including subsidies.

As has been noted by many people, the wholesale price of electricity is largely driven by the price of gas. However, what is less well known is that a significant portion of the price of gas-fired electricity is carbon taxes. As shown in Figure C, Ember now produce an interesting chart breaking down the fuel costs and carbon costs of gas-fired electricity.

")

In July 2025, they estimate fuel costs of £55.35/MWh and carbon costs of £24.87/MWh or 31% of the total. With Reform committed to ending net zero and flying high in the opinion polls, if they were to gain office then removing carbon taxes on electricity might be one of their first actions. Reform might also decide to reduce or eliminate Renewables Obligation subsidies.

If either or both of these actions were to occur, ORIT’s UK assets would suffer a dramatic and immediate reduction in power prices which would reduce their forecast revenues and make their assets uneconomic much earlier. On the continent, patience with Net Zero is also wearing thin; if other countries followed suit and cut carbon taxes, there would be a devastating impact on ORIT’s NAV as we shall see below.

Decommissioning Liabilities

ORIT says that estimated decommissioning costs are included as a cash outflow at the end of the asset life. As we have seen above, the asset lives are likely exaggerated and may well be shortened further if a new Government decided to end Net Zero and cut carbon taxes. Suddenly, expected positive cashflows from generation could turn into negative cashflows to fund decommissioning. However, there is no ring-fenced pool of cash to fund these liabilities.

Debt

The level of debt being carried by the group of companies that make up ORIT exacerbates the problems of rising discount rates, falling generation, optimistic asset lives, power price risks and looming decommissioning liabilities. In their accounts p52, ORIT says that at the end of 2024, debt was 45% of their Gross Asset Value. Any reduction in the value of the gross assets from any of the above risks pushes up debt as a proportion of the assets. ORIT appears to have recognised this risk and has set a target of reducing total gearing below 40% by the end of this year.

Combined Risks

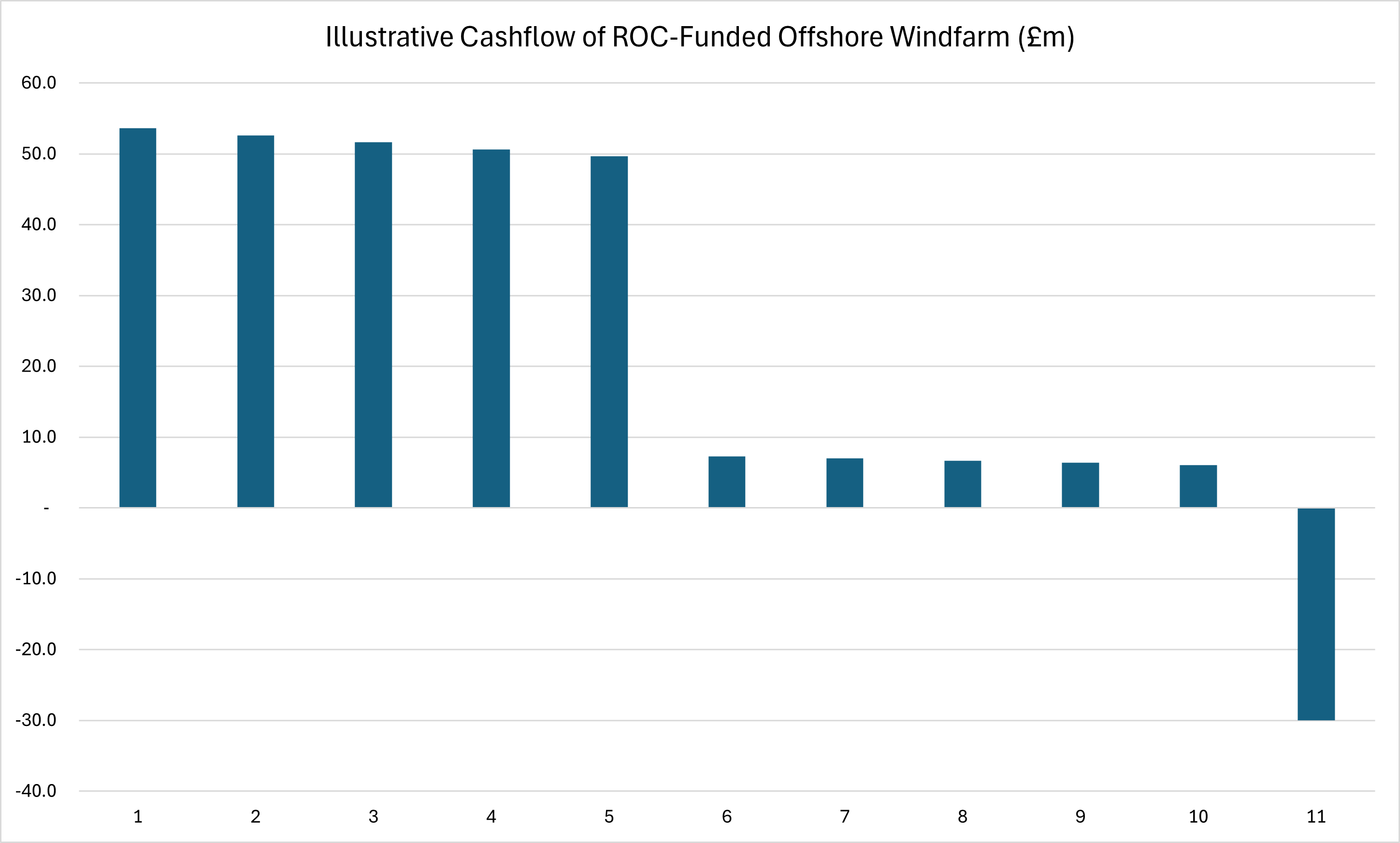

We can get a flavour of the combined risks facing ORIT and other renewables investment funds by considering a model of an hypothetical offshore windfarm. This model considers a 100MW, ROC-funded offshore windfarm with a remaining 10-year asset life, and a starting load factor of 40% with output declining at 1.5% per year. The windfarm receives 1.9 ROCs per MWh of output with five years of subsidies remaining. Operating costs are £14m per year, equating to £40/MWh in the first year. The market price of electricity is £75/MWh made up of £50/MWh gas costs and £25/MWh carbon costs. It is assumed the realised price for the windfarm is 12.5% below market rates at £65.63/MWh. Decommissioning costs are estimated at £30m in Year 11. The annual cashflows of this model are shown in Figure D.

Net annual cashflows start at £53.6m and fall slightly with declining output for the first five years. Then net cashflows take a big dive in Year 6 as the subsidies run out and eventually turn negative in Year 11 when the wind farm is decommissioned. Using a 10% discount rate the Net Present Value (NPV) of the first 10 years of those cashflows is £212.3m which represents the Gross Asset Value (GAV). If debt is 40% of GAV or £84.9m, then the base case Net Asset Value (NAV) is £127.4m. We can now work through the sensitivity of the NAV to decommissioning costs, a reduction in realised prices, increasing discount rate, the removal of carbon costs and the early elimination of ROC subsidies. The results of this sensitivity analysis are shown in Figure E below.

Including the decommissioning costs in Year 11 cuts the NAV by 8.3%. Reducing the realised electricity price by 10% cuts 10.5% off NAV and increasing the discount rate by 0.5% to 10.5% reduces NAV by 2.4%. Combining all three sensitivities reduces NAV by 20.5%.

However, things get very interesting if we consider what an end to Net Zero might mean. First, if carbon costs (Emissions Trading Scheme and Carbon Price Support Mechanism) are eliminated. NAV drops by 35%. Removing the ROC subsidies immediately sends the NAV negative and combining the two measures reduces the GAV to just £3m, but the £84.9m of debt sends the NAV plunging -£81.9m. Including the Year 11 decommissioning costs sends the NAV even lower to -£92.4m. In reality the NAV will be even lower because net cashflows turn negative in Year 7, which would bring forward decommissioning to Year 8.

Conclusions

In common with other funds focused on renewables, Octopus Renewables Infrastructure Trust appears to be adopting some rather aggressive accounting policies that have the impact of inflating asset values and probably under-stating the risks facing the company.

They benefit from fairly predictable income by harvesting renewables subsidies, but have loaded the company with debt, assumed asset lives that are far too optimistic. They also ignore the risk of a change in the political weather that could see Net Zero abandoned and their realised power price assumptions undermined if carbon taxes and subsidies are cut. Their NAV would be sent tumbling.

The falling share price perhaps tells us that the market is catching on to the risks surrounding funds of this nature. It remains to be seen whether its new roadmap for growth will deliver any benefits. For consumers, renewables have been a tragedy. Like with Shakespeare’s Yorick, one day soon shareholders might be picking over the remains of ORIT lamenting the good times of yesteryear. Regulators should be taking a greater interest in these retail funds.

This Substack now has over 4,600 subscribers and is growing fast. If you enjoyed this article, please share it with your family, friends and colleagues and sign up to receive more content.

I have been invited to speak at the Battle of Ideas Festival on 18th October on the subject of “Why is my energy bill so high?” You can get 20% off any ticket price by clicking on this link.

We moved our account to Octopus this month for two reasons: Scottish Power don't bother answering the telephone and their email support is useless but mostly because Octopus bill on a monthly basis. I want to know that my account is up to date, not based on some arcane quarterly arrangement.

Our utility companies generally seem to function on outdated models that just aren't rational for the modern world - much as the rest of the public sector.

The scammers leapt on the green con because it was easy money, forced from the tax payer by the state under duress. There was no risk, no cost to them, the returns were generous and guaranteed: all big fat state demanded was the technical expertise to force its stupid ideology on the public.

Now we have a farrago of clever accounting, plain deceit, obvious failure and the likely collapse of the hard left tax scam suddenly all that easy money looks to expose these absurd utilities to a real problem - and no doubt, yet again, the tax payer will be forced to bail them out to keep the scam on the road.

In other news, a chum recently considered solar. The only thing he didn't account for was energy getting 10-15% more expensive every year. It is utterly wrong that our grid, once so reliable, consistent and monetarily stable is now at the mercy of unreliable, inefficient, politically motivated tax scams perpetuated by liars, thieves and fools. Worse, these nonsense unreliables are doing real environmental harm, are not even owned by us for the capital return, are eyesores and represent nothing but the burning of tens of billions of pounds of money not put into creating real outcomes. They are socialism writ large.

As with the rail franchises, everything the state touches it ruins. Why can we not stop these fools doing this damage?

Brilliant analysis, offering depth, breadth, and detail surpassing what most asset managers access, yet fully comprehensible to the average reader.

Some company directors get too clever with their names, weaving in subtle in-jokes or irony. Could Greencoat UK Wind be an “ironic naming choice,” hinting at the practice of greenwashing a company?